February 2021

We are embarking on a very exciting year at Raba. Our founders continue to drive their enterprises toward solving hard problems. The result has yielded tremendous growth in 2020. We will host a Zoom call event in March to review the progress our founders are making (invites coming your way soon).

In 2021, we will continue to invest in three areas:

- Building deeper relationships with founders (the primary driver of our flywheel).

- Adding talented investors/founders/operators as Raba scouts and team members.

- Developing internal systems and processes to scale operations as we grow our team.

We will continue to invest in content to educate investors on the opportunity set in our geographies, as well as put together events that connect our founders with global investors.

2020 | an incredible year for technology

The performance of the technology investment sector has been — in one word — incredible. I’m more optimistic than ever that the next ten years of company-building in our ecosystems will be unprecedented and accelerating.

Over the last year, we’ve seen:

- Over $1 billion in exit value in African tech

- Companies like MercadoLibre, a Latin American ecommerce and marketplace company, reach $100 billion in market cap, after an IPO at <$1 billion in 2007

- Venture-backed NuBank, a digital bank in Brazil, grow to over 34 million customers and $25 billion in valuation, building a technology company in a market where banking rates and fees are extraordinarily punitive and customers are underserved (sound familiar?)

- Kaspi in Kazakhstan (a country associated with Borat movies for most) built a $12 billion fintech and marketplace company serving a population of 19 million people

- Fawry, a payments network in Egypt, reach a $2 billion market cap, up from $300 million a year ago. It is now the largest technology company listed on the local exchange, and has inspired a wave of young fintech founders in the region

While company valuations tell part of the emerging market story, there are a few metrics that really excite us. First, developer communities in Africa are booming, Nigeria recorded developer growth of over 170% in the last two years, and Google and others are investing to train over 100,000 developers on the continent. Data usage is exploding, and projected to reach 7 gigabytes per user per month in the coming years, up from 1.6 gigabytes in 2019. African ecommerce penetration is roughly 1% and cash payments in Africa amount to more than $1 trillion per annum, and a small fraction of payments are digitized. We can confidently say that payments and online transactions will be much much larger in the next few years.

Our reach, brand value and knowledge continue to compound with each successive company that joins the partnership. Our philosophy is to back founders early in their journey, with conviction, and to provide founders with the creative space to experiment and the confidence to move aggressively. We are proud of our work, but don’t take our word for it! We invite you to contact our founders to help you better understand how we operate — list of contacts here. We just ask you to be judicious with their time.

Portfolio update

We are excited to announce that we co-led (with our friends at firstminute capital) a $4 million seed round for Stitch, a banking API company building a fintech graph for Africa. The Stitch team’s ambition starts with connecting African fintechs and businesses to financial services providers via APIs. Stitch is often called “Plaid for Africa”, but this comparison understates the opportunity. We see the potential here as even greater, given the nascency of digital products in Africa. Remember, we are still mainly competing with cash and basic payments networks, as even credit cards have limited penetration. Today, consumers and businesses are woefully underserved by traditional financial services providers, as 40% of the population do not have bank accounts or access to formal financial services.

An important part of our value add to founders is our network. Today, our network is a group of 600+ founders, operators, and investors that span major tech ecosystems globally. The impact of the right network in our ecosystem can be a gamechanger for a young company. In 2016, after an initial angel investment in Flutterwave’s pre-seed round, we introduced the team to Iqram Magdon-Ismail, co-founder of Venmo (a thriving US fintech, acquired by Paypal). Iqram not only provided valuable early guidance to the company but ultimately helped Flutterwave land their Series A financing with Venmo’s early investor Greycroft.

We strategically look to introduce our founders to seasoned operators like Iqram who can have an outsized impact helping founders avoid pitfalls and navigate challenges. When we find people we like to work with, we look to do more of the same, and are excited to be working with Iqram on our mutual investment in Stitch.

Below, we share our thesis on why we are excited to deepen our partnership with Stitch.

Why we invested in Stitch?

We first met the Stitch team in 2019, and were excited about the idea of unifying payments and data via a single API. We moved quickly to set up a meeting with the founders — at our regular spot, The Blue Cafe. The founders were high-energy and deeply committed to the problem they were tackling, with deep domain knowledge. Stitch was conceived after building Wigwag, a peer-to-peer payments product, where they found that bank and account integrations were arduous and one-off, and a major deterrent to launching fintech apps. The lack of robust connectivity between consumers, businesses and financial institutions forced them to abandon WigWag and build Stitch to solve this infrastructure layer problem.

What was it that excited us about Stitch?

Put simply, it was the team, and their conviction in solving a particularly hard problem. Stitch is led by Kiaan Pillay, Priyen Pillay and Natalie Cuthbert, co-founders who have experience building and scaling successful technology companies. Kiaan (CEO) is a commercially oriented visionary who has demonstrated an ability to attract strong talent to the company’s mission. Priyen (CPO) leads product and has built products to scale, including at Flash, one of Africa’s most successful fintechs. Natalie (CTO) was a senior engineer at WhereisMyTransport, a fast-growing Google Ventures-backed startup. The broader team includes outstanding tech talent who have joined from other leading startups and technology companies — Amazon, Takealot (South Africa’s largest ecommerce company), Over, and Jumo (an at-scale venture-backed company that has raised $100 million in funding).

During our pre-seed diligence in 2019, we focused deeply on the technical side of the team and product. We worked with Symphony, a firm that prototypes and builds technology for early stage companies, to audit the technical talent at Stitch (we highly recommend their work). We also had an assessment and feedback session done by Jacek Migdal, a 10x talented software engineer who is currently an engineering lead at SumoLogic and prior Facebook. Jacek spent time with the Stitch team reviewing system architecture, and provided valuable feedback to the company. Further, a senior data engineer at DataDog (public enterprise software company) completed due diligence of the company’s API documentation, and was so impressed with the technical quality that he inquired about personally investing in the company.

As the product developed at Stitch, we kept a dialogue with prospective customers and tapped our network of fintech founders to gauge the significance of the problem. We learned that connectivity to data was often manual, tedious, time-consuming and prone to error. The demand for that connectivity appeared large, with no solutions on the horizon. In one due diligence call, a large enterprise bank reported using an external API provider to help connect internal systems. We became convinced that we are on the “right side of history” to be building a company like Stitch today. These unexploited markets and the quality of the Stitch team excited us enough to pre-empt raising a seed round.

But aren’t banks moving to open banking and creating APIs and isn’t this all kinda solved?

We believe this is the future of banking and that companies like Stitch are well positioned to serve the full range of financial institutions with the infrastructure to drive initiatives like open banking. In many ways, this follows the evolution of companies like Plaid in the US and now Europe, from building direct API connections to offering an exchange, a platform whereby Plaid provides tools to banks to offer such services. While it is very early days in open banking initiatives (especially in Africa), it will be important to continue to monitor the progress of open banking and build technology that can adapt to customers' needs (especially banks). Stitch is bringing on key members from Plaid as investors, and we expect to leverage those relationships as we move forward.

One of the reasons these initiatives are hard for banks (and most large financial institutions) is that they run their core systems on legacy infrastructure. As consumers, we don’t see the back end of the interfaces we use. While organizations continue to upgrade their mobile apps and online presence, they don’t do much to upgrade the core. Here is an excerpt on the subject from an article titled “Sorry for the inconvenience: Why your bank’s systems keep failing:”

“Every time there’s a new piece of technology, banks develop a front end addressing the disruption needs. But at the back end, you reconcile with the same system of records,” said the CIO (of a large bank).

For example, when a bank develops a mobile banking app, the interface may be a new application, but the app is still connected to the same database with the users’ bank records. This has resulted in a clunky and unwieldy system, where issues are hard to isolate.

In turn, it gets increasingly difficult to change any one function in the monolithic, inflexible IT infrastructure without upending others. “If any one part of the application has to be upgraded, the entire application has to be brought down,” explained the managing director of a cloud computing company who works with banks.

Read more here.

Internally at financial institutions, IT teams rather than software teams are managing these systems, and the increase in digital transactions creates stresses that amplify the issues. Stresses from the explosion in digital transactions have created huge market opportunities for API companies like Twilio, Stripe and Plaid. We wrote about APIs as a business model in July 2020, and since then Twilio, Stripe and Plaid have added close to $100 billion in enterprise value!

What does the market in Africa look like, and how defensible is it?

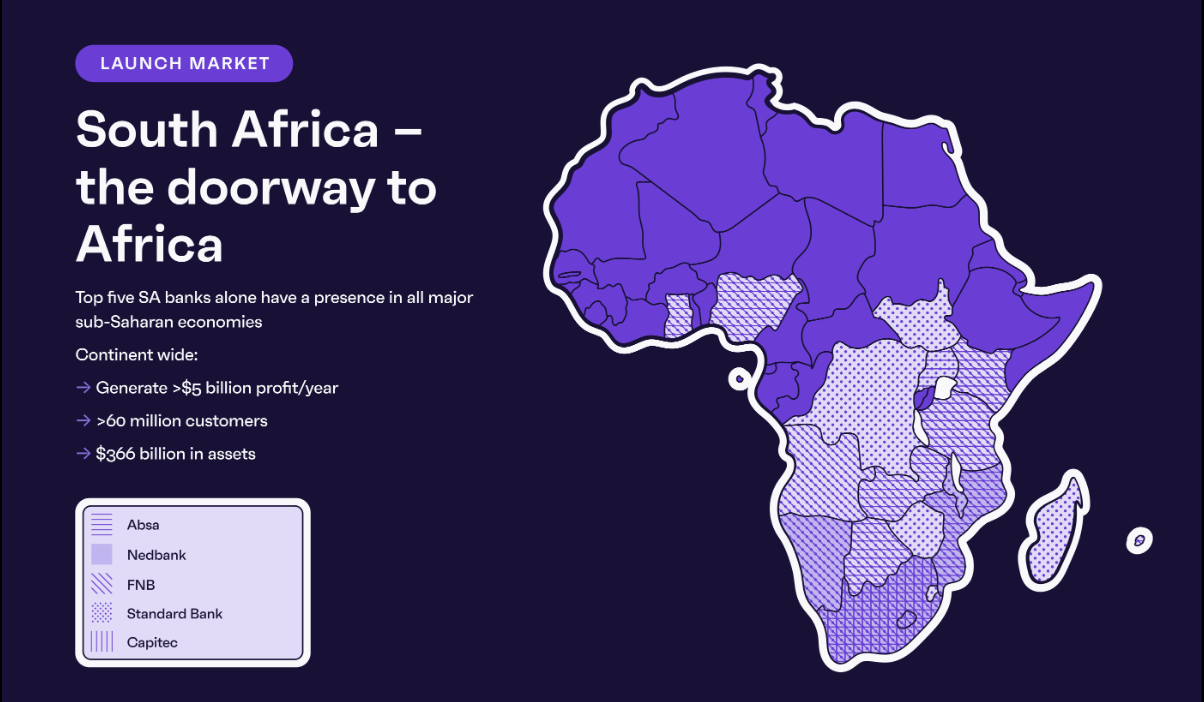

Stitch is initially focused on providing connectivity to South Africa’s five largest banks. As the infographic below illustrates, these banks are active in all of the major economies in sub-Saharan Africa. The connectivity infrastructure that Stitch has already established can be leveraged to gain distribution in the next eight to ten most strategic markets.

Stitch is building an increasingly important data layer and connectivity points (like Visa) that will be difficult to replicate. For example, Stitch can source and categorize a wide range of customer data from disparate sources (e.g., P2P payments app, bank account, savings app, etc.) to generate a uniquely price customer view that cannot be easily replicated. A key to the long-term defensibility of the business is having a data strategy and executing against it. By being in the API layer, Stitch works with customers who acquire necessary payments and banking licenses to offer their services to consumers and businesses. The Stitch API is effectively the plumbing that enables these apps to deliver their value — the ultimate sticky foundational software. The infrastructure layer is where there will be long-term defensibility and growth, enabling fintechs and larger enterprises with data and better tools to serve their customers. We outlined this case in our note on “Why we love APIs" — link here.

Exciting for Stitch and Cape Town!

Part of our mission is to continue to put Cape Town on the map as a burgeoning global technology ecosystem. It is exciting to continue to build bridges between global investors and the incredible teams building great companies in this part of the world. During our interactions with investors, we frequently heard their glowing reviews of the quality and depth of the Stitch team. Here is a quote from firstminute partner Arek Wylegalski: “Having been lucky to work with many great fintech founding teams such as Revolut, Raisin and Prodigy Finance, it became clear to me that the team behind Stitch is exceptional. They quickly established themselves as the talent magnet in their ecosystem and built a strong mission-driven culture. This is especially important when building tools for developers. We are excited to be on this journey alongside Stitch and to help them build this new layer of financial infrastructure." We at Raba are excited to welcome on board Arek and Sam Endacott at firstminute, Anne Dwane at Village Global, Aadil Mamujee at Musha, and strategic angels from Plaid, Coinbase, Paystack and Klarna.

Other news and musings...

Great Entrepreneurs are Stubborn Contrarians and Eternal Optimists is a fantastic post from 2013 and one of my favorites to read, and re-read. This piece by Marcos Galperin about entrepreneurship is as true today as it was then, especially for founders building companies for non-obvious markets. Marcos is the co-founder and CEO of MercadoLibre (which, as mentioned above, reached a $100 billion market cap). Here is a a great excerpt:

“I remember the first time I communicated my idea about starting an ecommerce marketplace in Latin America to my Latin American classmates at Stanford back in 1998. The overwhelming majority told me it would never work. They would say that Latin Americans don’t trust each other and hence, they will never buy something they have not seen or touched, from someone they do not know.... ’That behavior only works among Gringos!’ they would say.”

Sound familiar??