October 2020

It’s been an eventful last few weeks, with several announced exits in the African tech space, the most recent being Cape Town-founded Luno by Digital Currency Group. Many of the announced acquisitions were of fintech companies, including Sendwave (remittances) by WorldRemit for $500 million, DPO (payments) by Network International for $288 million, and Beyonic (infrastructure) acquired by MFSAfrica.

Exits play an important role in technology ecosystems, of course, especially in returning capital to investors who have business models predicated on exits to raise subsequent funds. Even more important is the psychological win for company founders and employees directly involved in these companies and especially for aspiring founders.

Forbes 40 under 40 in Africa

Forbes recently announced their Forbes 40 under 40 selections of emerging leaders across healthcare, finance, technology, government and entertainment. We are proud that three Raba company founders were selected and will brag a bit that they were the only three startup founders in Africa. Below are the awardees and their respective fields. Congratulations to our three founders!

- Abasi Ene-Obong // 54Gene - healthcare

- Olugbenga Agboola // Flutterwave - finance

- Obi Ozor // Kobo360 - technology

In this update, we review the South African market as an opportunity for fintech, and contrast it with Brazil (a market with similar characteristics to SA).

Why fintech in South Africa is an attractive market

The top five largest banks in South Africa (SA) generated over $6 billion in earnings last year — that’s profit, not revenue! This was achieved despite a recession in 2019 and the currency being at close to all time lows. The five largest SA banks operate with a significant cost base too with an average of 35,000 employees each!

To put these numbers into context, we compare the SA financial services market to Brazil, which has structural similarities. Both markets have near oligopoly-like characteristics where the largest five banks have over 90% market share and have (for a long time) charged high interest rates and fees — the largest bank in Brazil, Itau, generated over $5 billion in earnings last year alone. And even more importantly, both markets have large, underserved business (SME) and consumer segments that are mainly cash based, largely informal and make up 35-40% of GDP and employ over 50% of the workforce — a wide ocean of opportunity.

A deeper dive into the comparison of SA to Brazil

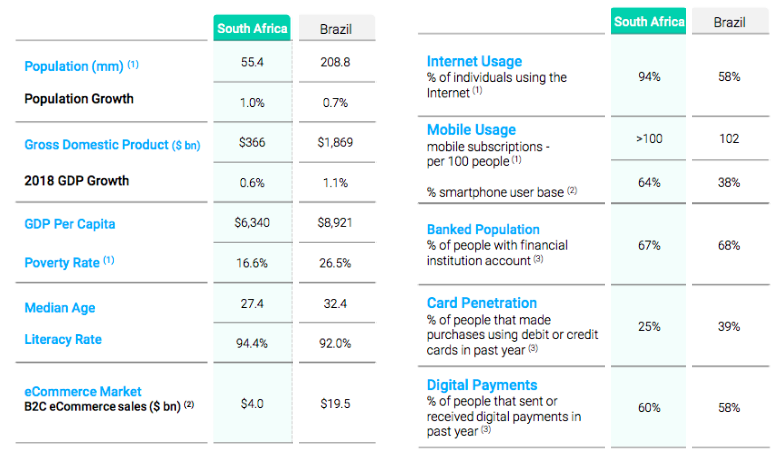

The infographic below (courtesy of FT Partners) is a high-level comparison of economic, demographic and fintech data between Brazil and SA.

You will note similarities across the two markets; banked population (67% vs 68%), smartphone penetration (64% vs 38%) and digital payment adoption (60% vs 58%). These “digital readiness” stats are comparable and favor SA. In terms of consumer income and spending, SA citizens are roughly at 85% of Brazil’s level on a PPP basis (PPP adjusts for what your local income can buy across a basket of domestic goods) and at over 70% on an unadjusted level. The obvious difference is scale, with Brazil having a population of about 4x that of SA. However, these statistics reflect only a partial view of the opportunity and miss the significant informal SME sector that exists — precisely areas that companies like PagSeguro and StoneCo in Brazil, which have built a combined $30 billion in market cap value, have focused on.

It’s about funding

Brazilian fintechs like NuBank have raised over $820 million in VC/growth equity to pick apart the banking profit stack with a lower cost operating model that allowed them to provide superior service and growth as they focused on opportunities in underserved channels. Nubank today serves over 25 million customers with 2,700 employees vs. Itau (Brazil’s largest bank) at over 82,000 employees. The entire cost structure and operating model is different — technology on one side vs. legacy banks on the other.

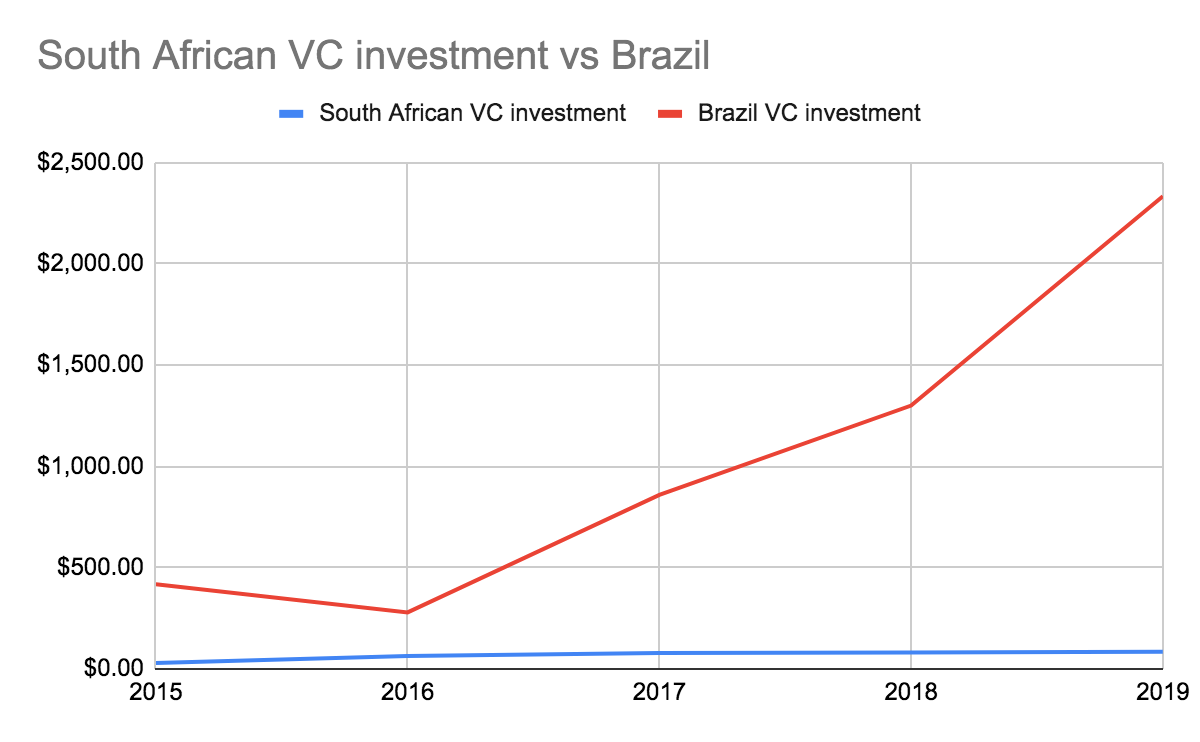

We’ve prepared the graph below to show how stark the funding difference between SA and Brazilian VC investment has been over the last 5 years. In 2019, Brazilian companies raised more capital in ~8 weeks than South African companies have raised over the last 5 years. It’s hard to build companies without risk and growth capital.

Why is this the case? It’s part investor perception, regulatory environment, timing, and exits — fintechs StoneCo and PagSeguro successfully IPOed in 2018. Further, many exciting fintechs in SA were acquired by banks — when a founder is faced with limited growth funding (as outlined in the graph above) and an acquisition offer is there, it’s hard to pass that up. The Silicon Valley founder can pass on an early acquisition offer and continue to build — knowing they have growth and later stage capital partners to fund them — for an even larger outcome. Brazilian fintechs have been able to close that gap with local and international investors and we believe SA is poised to do the same. It’s part of our mission at Raba to bridge that gap between world class investors across markets and company builders in SA.

Closing thoughts

If we view SA as a smaller version of the Brazilian market, with significant growth in the informal sector, can we conclude that we are on the cusp of building large technology-driven fintech players in SA? The short answer is, yes. We believe companies like Yoco (a Raba portfolio company) have the opportunity to build defensible software-driven financial services businesses that can be standalone public companies, maintaining a focus on the SA market for their growth. SA has the largest financial services market in Africa, making it a natural base for expansion — playbook that many SA companies have successfully executed.

Other news

Snowflake, company incubation as a differentiated venture model? As we evolve our internal BUILD program at Raba (where we are a founding investor and help commercialize ideas), this piece on Mike Speiser’s “playbook” at Sutter Hill was a really interesting read. Mike was a founding investor in Snowflake (that recently went public and has a $60+ billion market cap) and is involved with several other notable companies. I believe many of you (especially the VCs) will find this article illuminating.