November 2020

We’ve doubled our headcount!

I am excited to announce the addition of Nina Chen as our new investment associate. A bit about Nina — she grew up in Toronto, graduated magna cum laude from Harvard with a degree in social studies, and joined management consulting firm Bain & Company in New York. In 2018, she moved to Zambia for a Bain-sponsored externship at TechnoServe, and decided to stay in the continent, moving to Nairobi last year as the Director of Growth at ALX (African Leadership Academy). During her last few years working in Africa, Nina has built a network of relationships with startup founders and operators (that’s w we got introduced), and that experience and her analytical acumen make her a strong fit for Raba.

I look forward to introducing Nina to you in the not too distant future.

Raba Partnership Annual Call

We will be hosting our inaugural Raba Partnership Annual Meeting as a Zoom call next week. Several of our portfolio company founders/CEOs — including 54Gene, Cloudline, Lori Systems, Stitch and Yoco — will provide insight into their businesses and opportunities they see.

Invitations were recently shared via email.

In this review, we share thoughts on using data to solve customer problems and to expand into adjacent business opportunities. We think this focus is particularly relevant for early stage company founders, and invite your feedback on the topic.

Solve a core problem then solve others...

In many early stage company presentations, you will see a page on TAM (total addressable market), and it’s usually a big number ( billions of dollars). If the company can just capture x% of that market, well, the outcome would lead to something really really big! You might assume the founder did extensive work to understand the market and further assume they were going after the opportunity because it was big and important, right?

Not really.

We’ve observed too many early stage founders drawing up market size with oversimplified heuristics, it’s a mistake. We love big market opportunities, but that top-down approach is rarely actionable, and often misleading. Start with how many customers are in your target market and what you think customers will pay for solving that specific use case. Focus on a core initial use case (it’s ok if it seems narrow, for now) and make the product/service so good that a customer wouldn’t conceivably go back to the way things were done before.

Early use cases and data as a long-term advantage

Ideally, the early use case you’re solving generates a data layer to give you visibility on your customer which in combination with their feedback will help drive your product roadmap. This is particularly important for first time or less seasoned founders where they don’t quite have the muscle memory around identifying adjacent opportunities and/or how to build a data strategy to get there. This is also where early stage investors can add extensive value to bring on advisors and staff to complement the founding team.

As mentioned, we don’t get too worried if the first use case appears “narrow.” Instead, we think about the level of customer pain that we’re addressing, and the data we’re able to generate through our proposed solution. (I’ll write a seperate post on the importance of data layers as a competitive advantage). Having spent time with successful founders, I believe this early focus on data is the key differentiator in most companies, especially fintechs. Founders and teams that are data literate and connect that data to business decisions and outcomes build not only better businesses but more defensible ones too.

Square: An example to help illustrate the point

Let’s review Square as an example of starting with a single core use case (card acceptance), building data on your customers (through processing their transactions), and expanding service offerings (like offering small loans based on data). I’ve included a photo of the various generations of Square’s dongles below to show how a 10-year-old company achieved an $85 billion dollar market cap. The dongle allowed any small business owner with a smartphone to accept card payments in a low friction way by transforming a phone into a point of sales tool. In the course of solving card acceptance, Square was building the foundation for their future product roadmap as well as a platform for the services they could upsell to their installed base.

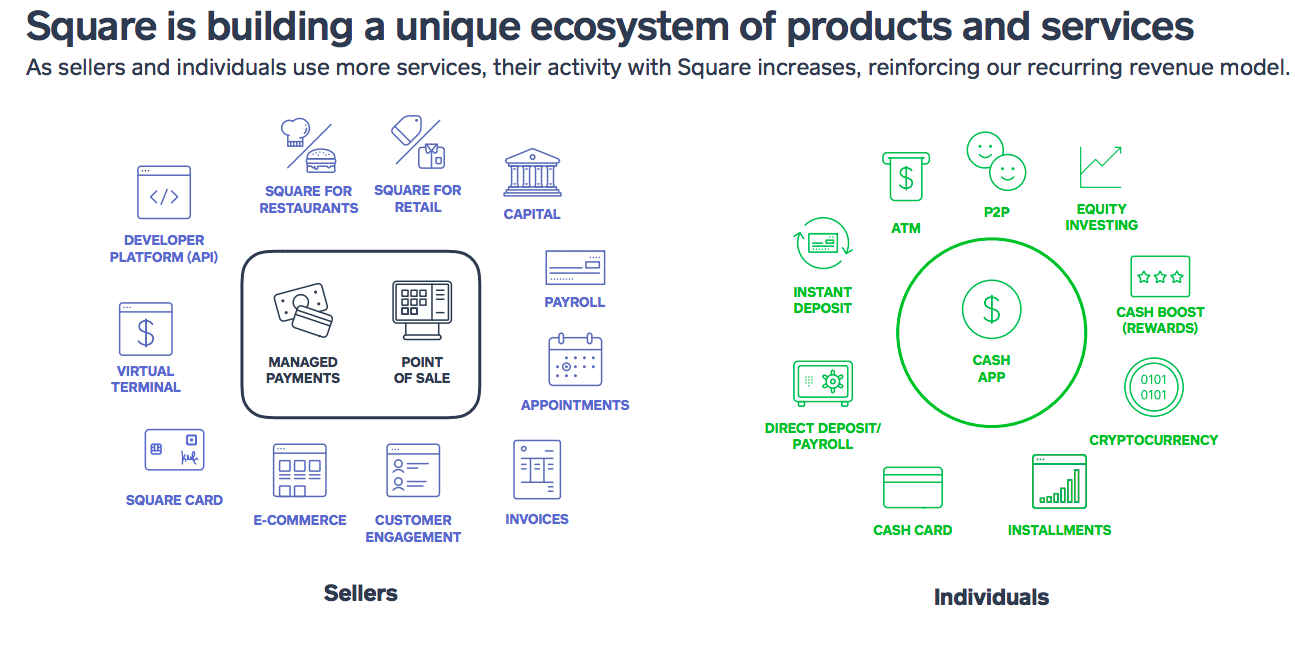

The infographic below from Square’s annual report dramatically demonstrates the breadth of their offerings. They include company payroll, ecommerce, invoicing — effectively an operating system for your business that generates even more data for Square. Square can now track how much you pay suppliers and employees, producing data for additional product launches. While this all is happening on the merchant side, Square has been building the Square Cash ecosystem for consumers, and this is where things get really interesting. It can lead to what mPesa built in Kenya — a closed payments loop where consumers and merchants use the same platform. Since the payment does not cross Visa’s or Mastercard’s network, Square like mPesa owns their own loop and won’t share fees. In short, using data to drive strategy can drive a successful flywheel effect, as adjacent services collect even data and further drive that flywheel.

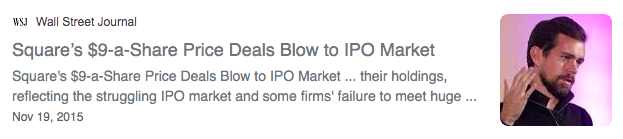

Interestingly, this data-oriented strategy (though pioneered by groups like Capital One many years prior) wasn’t obvious to investors. When Square filed their IPO in late 2015, it didn’t get much love, per the WSJ headline below.

Square’s shares recently traded at $200 per share.

How is this relevant to our focus markets?

Each market has its own nuances and requires adapted versions of a playbook. But we firmly believe in the idea of solving a core need, generating data, and expanding to adjacent opportunities by connecting data to business decisions. Most incumbent/legacy firms don’t have the internal culture to do so and generally lack the necessary talent to seize the opportunity. It’s especially hard to retrofit a legacy technology stack, an issue that is particularly acute for banks, despite being the largest spenders in IT services globally. We believe we have a unique opportunity to use global playbooks to build modern fintech companies where it will be even harder for incumbents to compete.

Other news and musings...

Where are all of the giant Chinese SaaS companies? Given our interest in software business models (and Africa), this analysis is an interesting deep dive on thinking through software business models in markets outside of traditional SaaS markets like the US and Europe. Link to the post here.