Hello from Cairo. 🇪🇬

It was great to host our founders, partners and friends in Cape Town for the third Stitch x Raba summit. One of the most rewarding benefits of this annual gathering is seeing founders and partners who met at previous summits turn initial conversations into business partnerships and even friendships. A big thank you to all who made the time and effort to join us. Based on the feedback, we will continue to invest resources to bring this group together.

Frameworks + themes:

We presented an update on our framework for investments and what we believe are the key ingredients, particularly for fintechs in emerging markets. Here is a summary:

- There are significant market opportunities to build dominant software-led companies in non-obvious, less tech competitive “small” markets. We reviewed Kaspi and Capitec.

- Having a clear regulatory strategy early in the lifecycle of a company is critically important. Licenses unlock your ability to leverage software and data to build next generation financial products. They also mitigate risk and create a competitive moat to drive differentiation and ultimately profits.

- It takes time. Founders and teams are compounding many small advantages to drive results over 10 or more years. Urgency matters, but there are no shortcuts.

We also shared our thoughts related to the significant currency depreciation faced in certain African countries, particularly Nigeria and Egypt.

An important moment in time for fintech in non-obvious markets

Our long-time readers will remember Kaspi, a Kazakhstani financial services company that we first wrote about in February 2021. Since then, Kaspi has grown significantly and scaled a business in a country with about 1/3rd of the GDP of Ohio. On the surface, it would be deemed a very small market. On January 19th, Kaspi made its US debut through the company's public offering on Nasdaq. In a time when public market liquidity has been challenging, Kaspi raised $1 billion in capital and listed with a $17.5 billion market cap. It was the largest capital raise since Birkenstock’s IPO (Birkenstock raised $1.5 billion at a $8.6 billion market cap). Since its IPO, Kaspi has added over $4 billion in market cap, or 50% of Birkenstock’s total value (which has been built over a long period, as it was founded in 1774!).

Even more impressive are Kaspi’s financials. The company generated $664 million in pretax profit on $1.26 billion in revenue in the fourth quarter alone, with revenue growing 45% year-over-year. As a comparison, Adyen, a global payments leader, generated $314 million in pretax profit on $490 million in revenue in the same period, growing 23% year-over-year. If public markets are the ultimate arbiters of price discovery, Kaspi’s success should provide a roadmap for venture investors, the possibility of building large businesses and generating returns in “small” markets. However, this will take time. When we reference Kaspi to global growth investors and friends who manage public equity portfolios, most have not heard of the company. The listing (and continued success) as a US-listed public company will change that. It takes an example to validate what is possible, and now global investors can scrutinize Kaspi’s financials every quarter and build their own mental models.

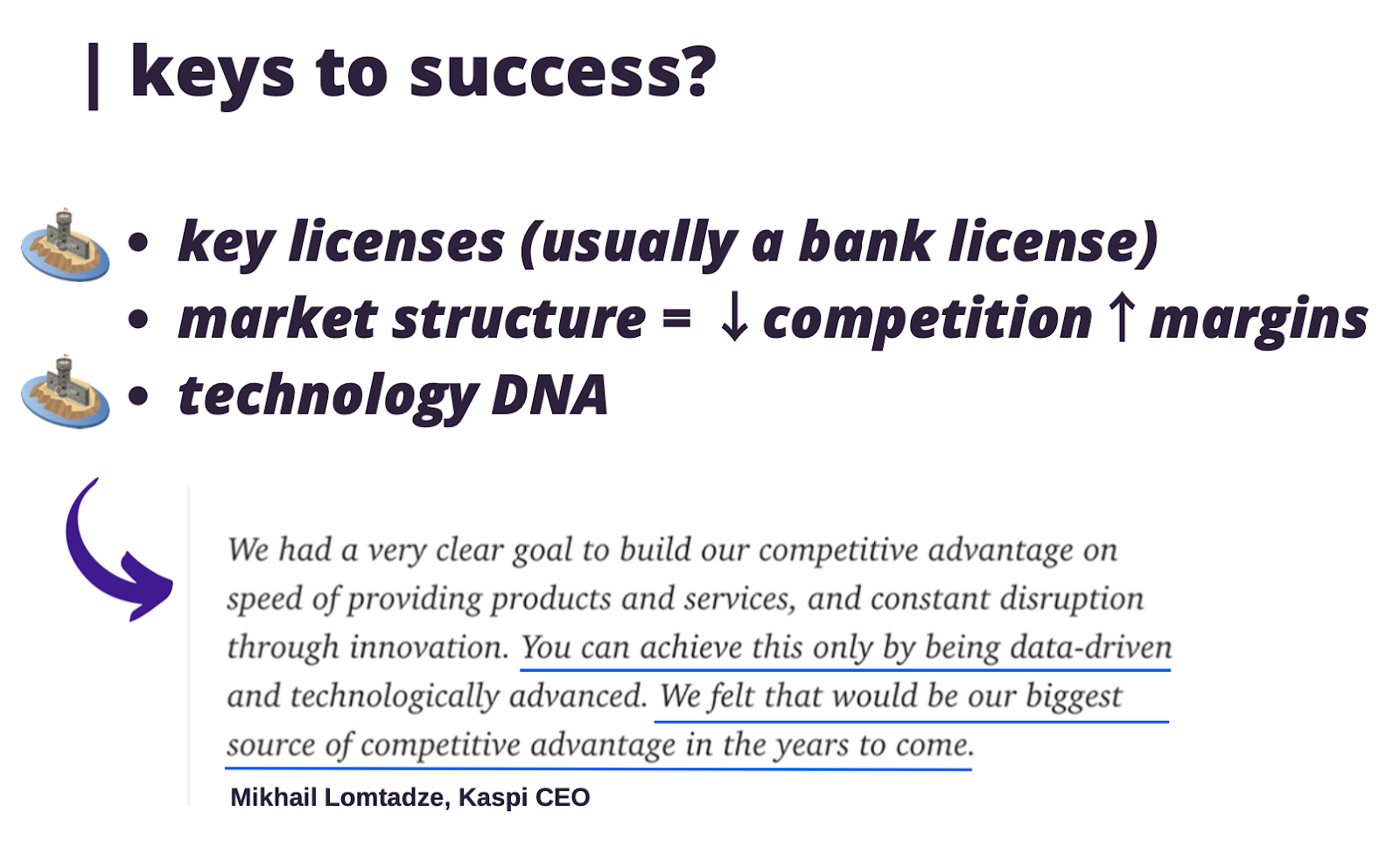

By studying these success stories, we formulated our keys to success for software-driven financial services businesses. Rather than a single factor, our model calls for an integration of three foundational elements: regulatory licenses, a market structure with legacy players that are not technology first, and a management team focused on leveraging software and data to build superior business models. The playbook will continue to evolve, but we believe these pillars will remain central.

Many emerging markets have one of these core ingredients – a market structure with highly profitable legacy competitors for which technology is not core to their DNA. Pairing that market opportunity with founders adept at navigating regulatory affairs is a necessary condition for success — this is one of the key learnings we have from our years of operating. We’ve seen many companies flounder or fail because they don’t prioritize licensing in the company's early building phase.

Building value in a depreciating FX market

It has been a volatile period for emerging market currencies, especially for the Nigerian Naira and Egyptian Pound. Over the last three years, the Naira and Pound have depreciated by 69% and 67%, respectively, vs. the US dollar. Both countries had what are known as parallel FX markets, where the official rate deviates significantly from the market rate. This created a difficult operating environment for businesses and stifled institutional investment and capital into the country. Both central banks moved to float their currencies, allowing the official rate to converge with the market rate, and leading to steep FX devaluations. All of which leads to uncertainty as to where we go from here.

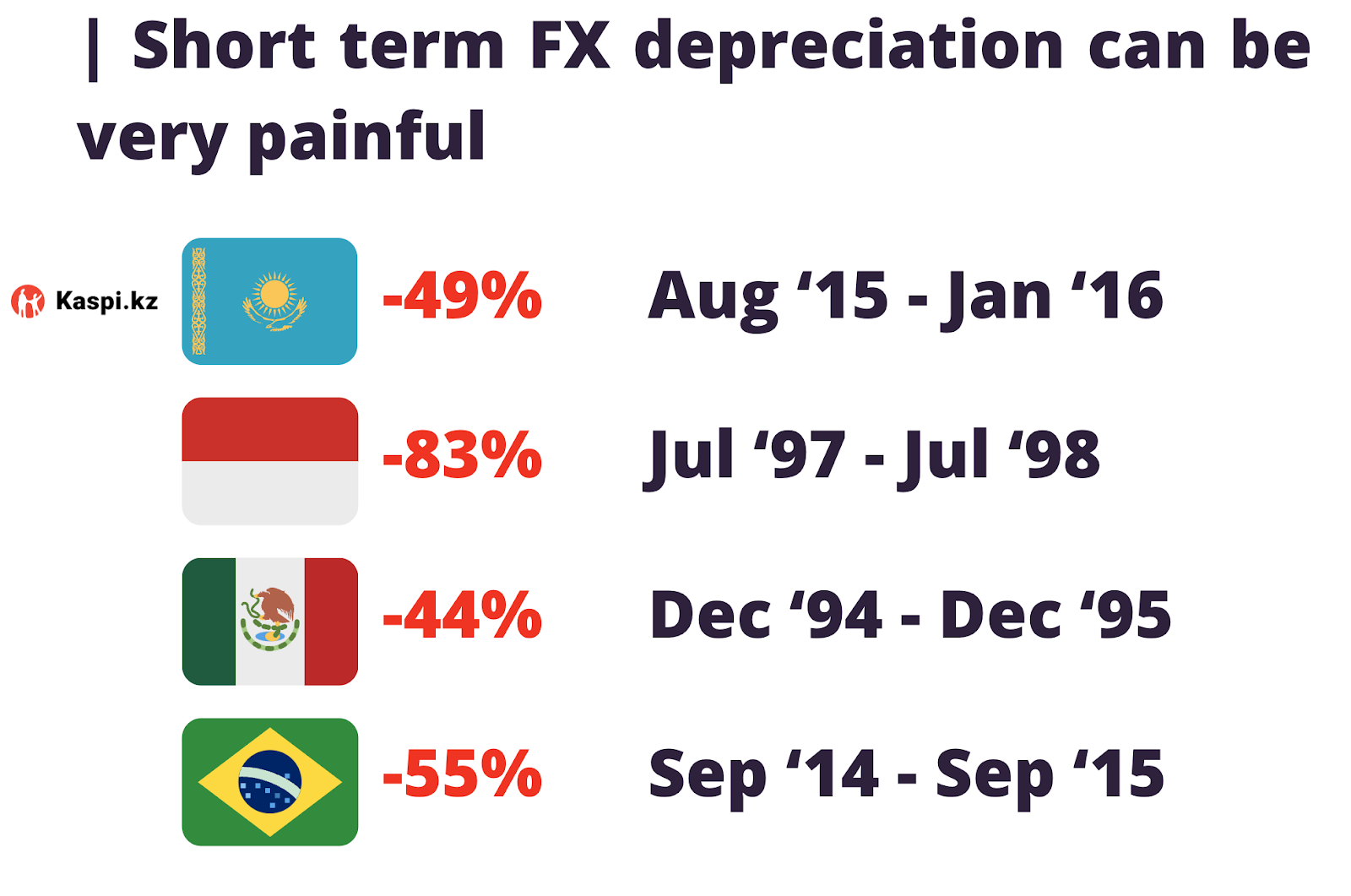

Below are four emerging market currencies that had dramatic one-year devaluations vs. the US dollar.

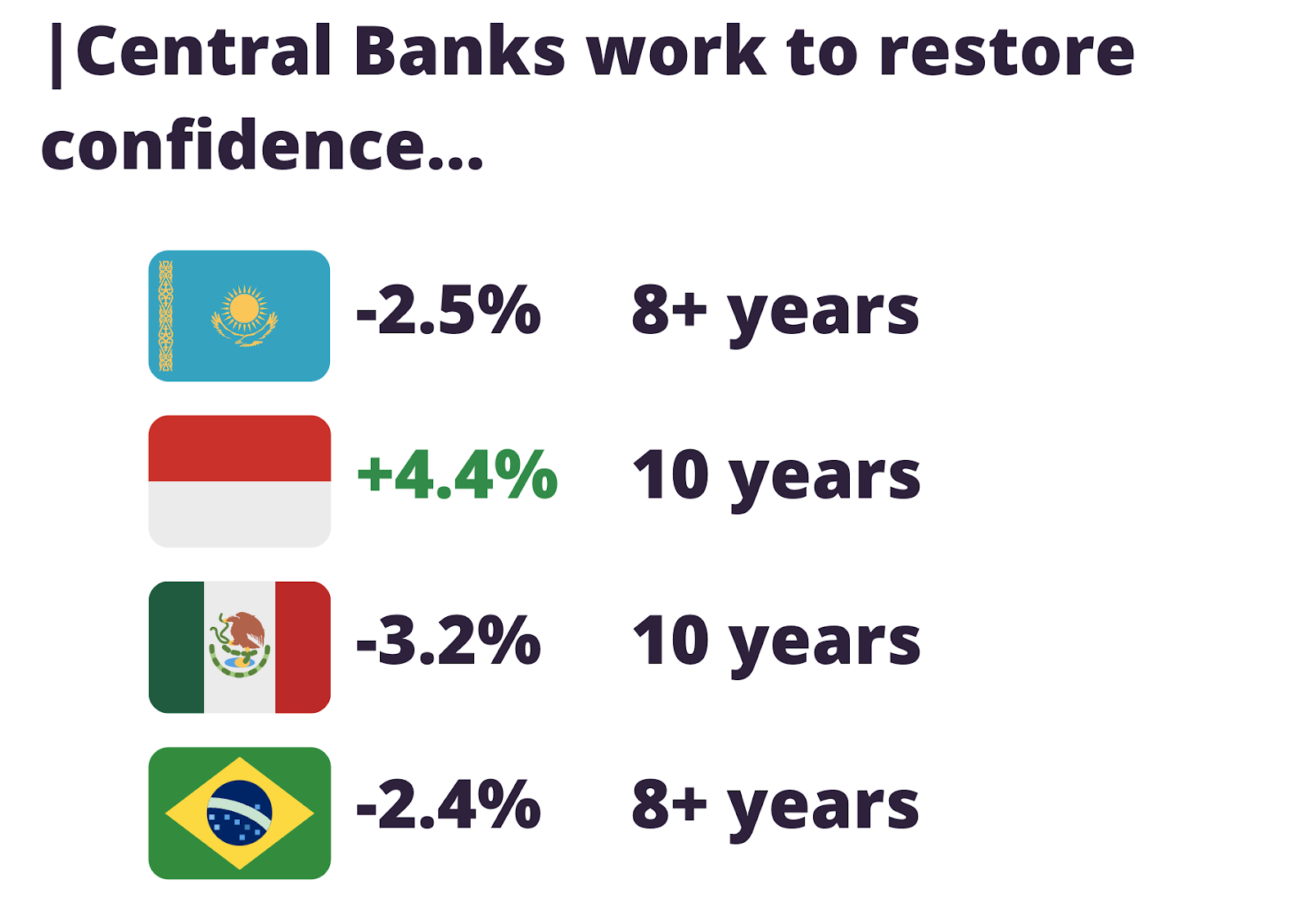

It’s not our expertise to speculate on currency movements. Rather, we’ve studied times of significant FX depreciation and examined how those currencies performed over a ten year horizon (figures below show the annualized appreciation/depreciation vs. the US dollar). In all four cases, the currencies were relatively stable vs. the US dollar in the succeeding ten years. Over a twenty year period, the Mexican peso and Indonesian rupiah were even more stable relative to the dollar.

Stabilization is in part driven by intervention from central banks. A similar case was Mexico in 1994, when the central bank floated the currency, prompting a severe bout of depreciation. Floating the currency was conditional for an external capital infusion from a consortium of the IMF, the US and other parties totaling $50 billion (see this Federal Reserve Bank of Richmond

piece). A similar storyline is playing out in Egypt today, where the Pound was freely floated earlier this year, and investments of $57 billion (12% of Egypt’s GDP!) followed from the Abu Dhabi sovereign fund, the IMF and the European Union. This has stabilized the currency, paving the way for structural reforms to enable efficient growth. An intended consequence is that a stable currency allows the government to raise local currency bonds, reducing dependency on foreign currency borrowing.

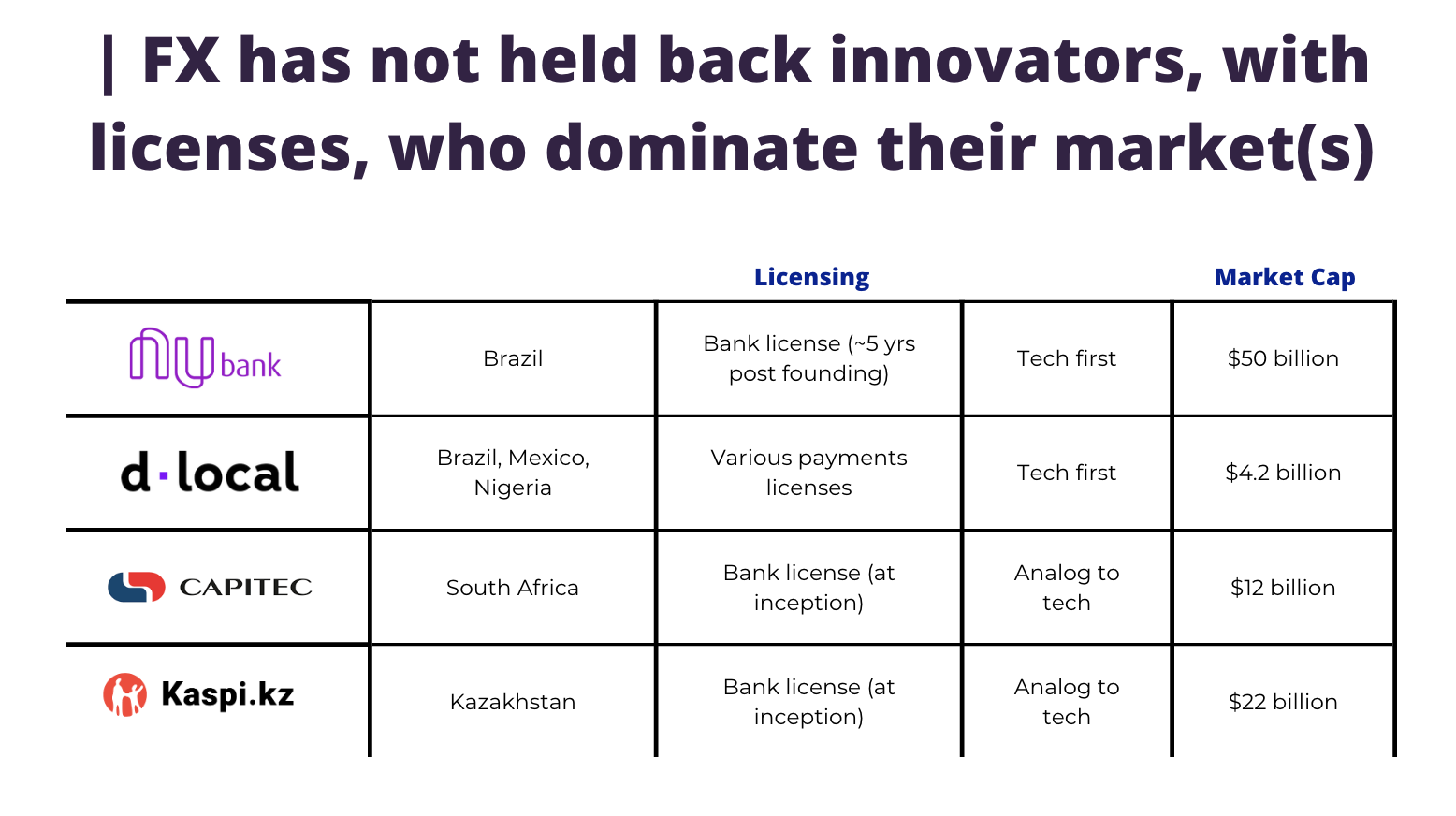

An ongoing question is whether companies can grow and generate enterprise value in US dollar terms in countries with structurally depreciating currencies. We believe that the answer is yes, that the combination of market structure and structurally higher margin business models more than makes up for depreciating currencies. Below are four examples of emerging market financial technology companies that have built significant value in the face of currency headwinds. Our estimate is that these companies have raised $5.6 billion in private capital to build $88 billion of market cap value and over $3.4 billion in profit in 2023.

Why business model matters

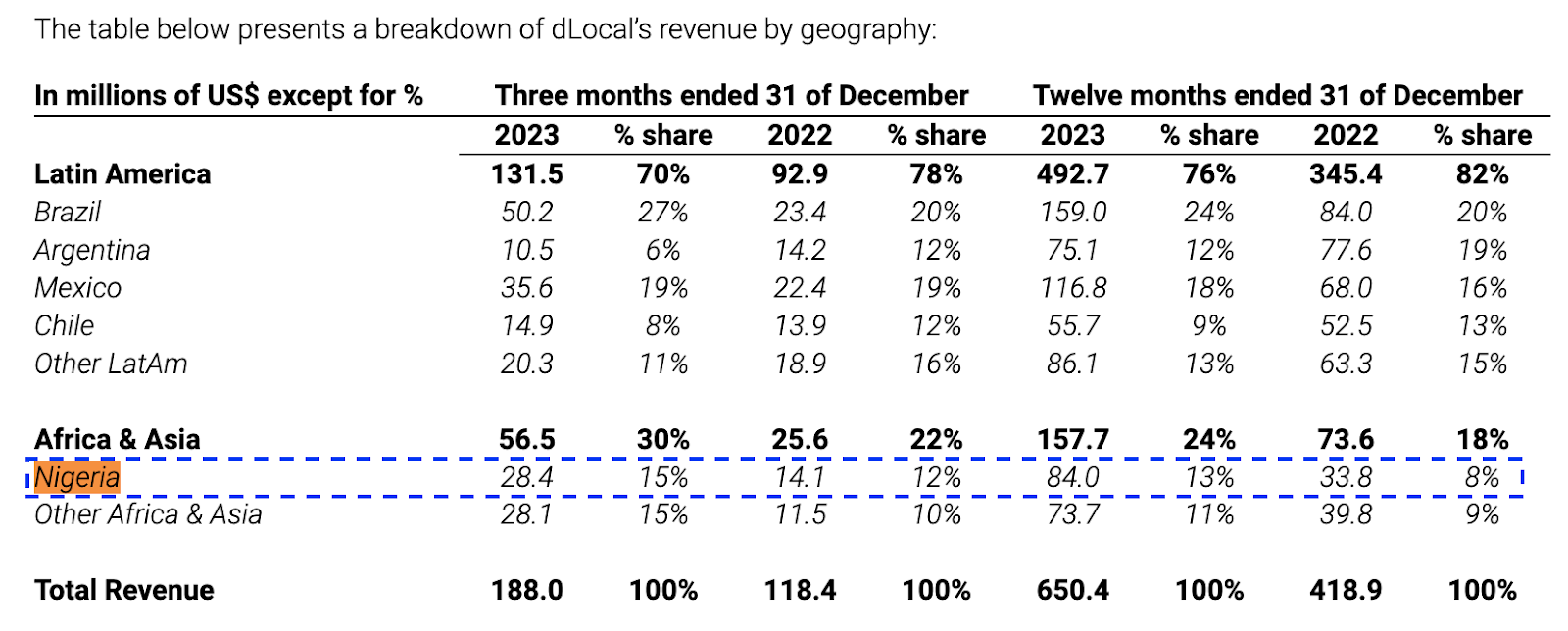

Business model matters – and payments companies are good examples – are uniquely positioned for FX depreciation, as goods and services are repriced with FX fluctuations. The flip side, of course, is that demand declines as the price of services increases. Business model decisions that management pursues are critically important. For example, a payments company providing local payment collection and disbursement for global multinational companies operating in non core markets should incorporate an ability to repatriate funds back offshore (presenting another payment to monetize). These various legs of money movement are important business model decisions that companies like Flutterwave and dLocal have built to great success. To showcase the power of these models, below are dLocal financials from the most recent quarter. The blue highlighted box shows that despite the significant devaluation of the Naira (49.3% in 2023 vs. the US dollar), dLocal grew US dollar revenues by 148%, from $33.8 million to $84.0 million.

Perceptions and things are better than you may think…

Below are statistics cited by Christo Wiese, widely considered one of the most successful retail entrepreneurs in Africa. He made these observations regarding South Africa today vs. years past:

- In 2002, life expectancy was 55 years old; today it is 63.

- In 2007, there were 4.8 million individual taxpayers; in 2021 there were 24 million; business taxpayers increased from 1.2 million to 3.1 million.

- In 1994, the budget deficit was 4.9%; it remains at that level in 2023.

- The ratio of total population to nurses improved from 340 to 200.

I share these observations to offset some of the negativity surrounding South Africa. Christo’s sensible thinking and data present a contrasting perspective worth attention. You can listen to his full podcast here.

On the subject of perception, this observation from Oxford economist Max Roser stood out to me. Despite statistical evidence of significant decline in global extreme poverty, 90% of people in the UK and 95% in the US don’t know things are improving.

- Even the decline of global extreme poverty — by any standard one of the most crucial developments in our lifetime — is only known by a small fraction of the population of the UK (10%) or the US (5%). In both countries, the majority of people think that the share of people living in extreme poverty has increased. Two thirds in the US even think the share in extreme poverty has ‘almost doubled.’ When we are ignorant about the basic facts about global development, it is not surprising that we have a negative view of our times and that few have the hope that the world can get better.

You can read Max’s full piece and follow his observations on global development at www.ourworldindata.org.

We met with the SwypeX team and our friends from Accel and Foundation Ventures in Cairo, ahead of their company's product launch. (See photo below.)