What are the core elements of a great business?

Is it what ends up getting funded by venture capitalists — strong revenue retention, user growth, revenue growth, margin structure, great team, predictability of revenue, durability? We have found investors offering a range of advice to founders — all of it seemingly well intentioned. But some misses the mark.

What should founders building software and internet companies in emerging markets be striving for?

The last decade was (as David Epstein, author of Range — a book we recommend — would describe) a “kind learning environment” for venture-backed founders. The playbook was to focus almost exclusively on increasing revenue, and funding will come. But not all revenue is created equal. Funding was a badge signifying success, and in some ways it still is. At the earliest stages, treating funding rounds as the primary benchmarks for success has been industry practice for early stage companies for decades, and is largely the same globally.

Where we want to present a differing view is in the domain of companies that have found product market fit and early signs of scale. We believe that founders and investors should consider deviating from standard venture practice, and focus on balancing growth and profitability earlier than what is conventional in other markets. We call it growth at a reasonable cost. This shift in thinking raises other questions. What is the balance? At what stage should companies focus on balancing growth and profitability?

It is about business fundamentals and your market structure

We invest in software and internet businesses, and this informs our thinking on where to find this balance. The power of these models is their ability to scale and their inherent operating leverage (revenue and gross profit grow faster than operating costs). This will likely be even more pronounced going forward, with the adoption of AI co-pilots/tools. In the early days of a company's life, investment is made in building a team and product, and testing with customers to find product market fit (largely the same globally). As you start to grow revenues, you generally raise capital to accelerate growth and extend your product portfolio. As you approach and surpass $10M in annual revenue (assuming stable gross margins of 50% or higher), you face a decision fork:

- Option A. Raise more capital to accelerate your path to “win the market”; or

- Option B. Pursue compounded growth balanced with profit to “win the market”.

For companies that are building in less developed venture capital ecosystems, path B should be carefully weighed. There is a path where founders can still “win the market” using the internally generated operating profits of the business. This approach preserves more ownership for early investors, employees and founders. It is largely enabled by a market structure where you rarely compete with other well-funded growth stage venture-backed companies (that are able to make uneconomic short-term decisions and blunt your ability to scale). Industry structure and your company’s competitive position are the fundamental differences.

But how? First, revenue retention

A metric that should be brought up in each board meeting is revenue retention — are we keeping good customers, are we growing revenues with them, and do the unit economics make sense? We’ve come to appreciate retention as a core driver of long-term value and believe it is imperative to measure it and refine your product for retention early. If you’re a founder, you should build this into your company’s DNA early. In the context of B2B companies, a baseline of 100% revenue retention is a good starting point. For companies serving enterprise customers, the baseline is higher. For example, dLocal (emerging markets enterprise-focused payments company) reported net revenue retention of 141% this past quarter and 157% the quarter prior.

Second, growth and profitability; Rule of 60

We have observed that companies with strong revenue retention, $10M in annual revenue, and stable/high margins (of at least 50%) are able to operate at or near breakeven with strong growth (2x-3x YoY). Instead of kicking off your process for a fund raise, we suggest a longer-term growth strategy — a 5-year plan. What is good growth in that context? We believe a company should target the rule of 60 — the sum of your topline revenue growth and profit margin (in these still early innings, we advocate focusing on compounded growth over near-term profit). This is an adaptation from the software “rule of 40” for mature at-scale businesses. While a 60% annual growth rate can 10x your annual revenue in five years, reaching $100M from $10M, we know some companies grow even faster (we have such companies in our portfolio today). We don't want to stifle ambitious growth aspirations. Instead, our focus is on ensuring the quality and durability of your growth, both today and in the years ahead. By setting in motion a focus on retention, continued product development (see below section on 'no resting on laurels') you chart a consistent path to compound growth without infusions of capital. When times get tough (as they often do, especially in less developed venture markets), you will be in a stronger position to control your destiny.

No resting on laurels…

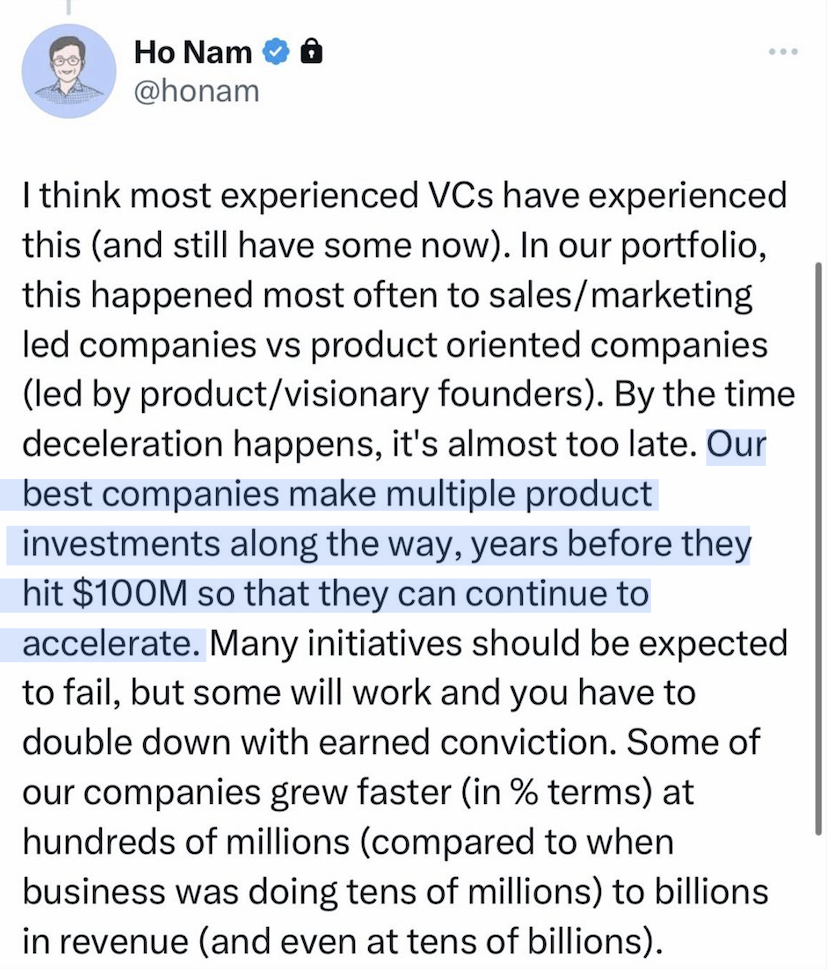

To sustain your growth and strong economics, the product engine does not stop. You will need to develop second and third acts — high retention from existing products will give you an opportunity to solve existing customer challenges with additional products. This is the definition of becoming a platform company, where customers consume more products and in turn are longer tenured customers (driving even higher retention). Becoming a multi-product solution erects a business moat which builds enterprise value. The retention and product flywheels are set into motion by establishing high retention early and building on that base. The twitter post from Ho Nam of Altos Ventures captures this point clearly (highlighted).

In short, focus on developing your retention and product muscles early and create specific incentives for your team. It will pay long-term dividends.

A story of compounding…

The prospect of hyper-growth is generally limited to global consumer internet companies — think Facebook and LinkedIn. We’ve studied companies across Africa that pursued similar charters with business models that operate in regulated domains and/or have high operational intensity and high capital needs. In most cases, the founder(s) was advised by investors to expand into new markets, as those investors considered any single country market in Africa to be just too small. We believe that that’s a fundamentally wrong strategy. Business models often don’t translate across borders, and the right business model in a single market can offer incredible opportunities to build value. We are comfortable trading market share vs market size.

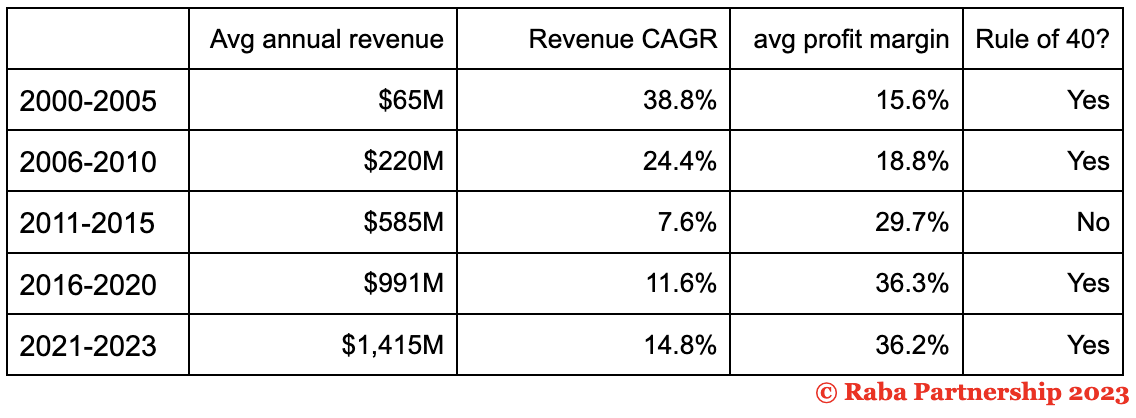

Below is a table of a single market compounder, Capitec, based in South Africa, which today has a $12.4B market cap. Each row represents a five-year period since the company's founding. Notice the compounded growth rates and profitability along the way. (All figures adjusted to dollars. Growth rates for Capitec were meaningfully higher in local currency terms. For context, the Rand was 8 to the dollar in 2001 and is now 19.)

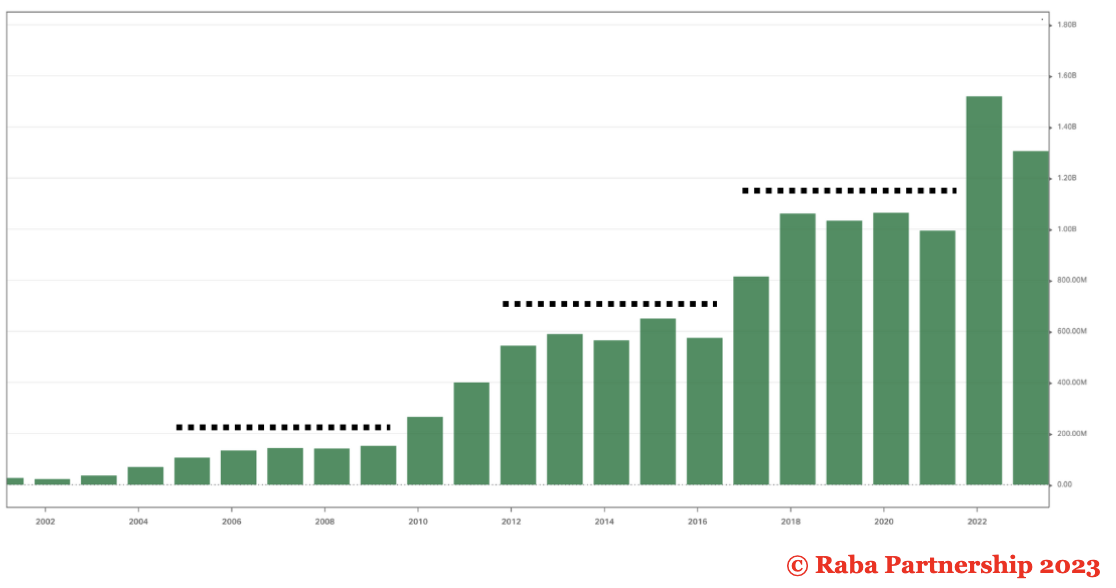

Below is a chart of Capitec revenue in USD. As you can see, there were periods where growth appeared to flatten (especially during periods of FX depreciation). However, the company continued to grow its customer base and serve them with an increasing array of products to overcome FX headwinds over the long term. This was possible due to the strength of the business model and high customer satisfaction (as evidenced by their high retention). Capitec has been a fixture atop consumer satisfaction surveys in South Africa. Also, the company did not hold back on investment. Capitec’s employee base grew from 1,792 in 2001 to 4,159 in 2005 to 10,450 in 2010 to 15,234 in 2023.

Capital efficiency

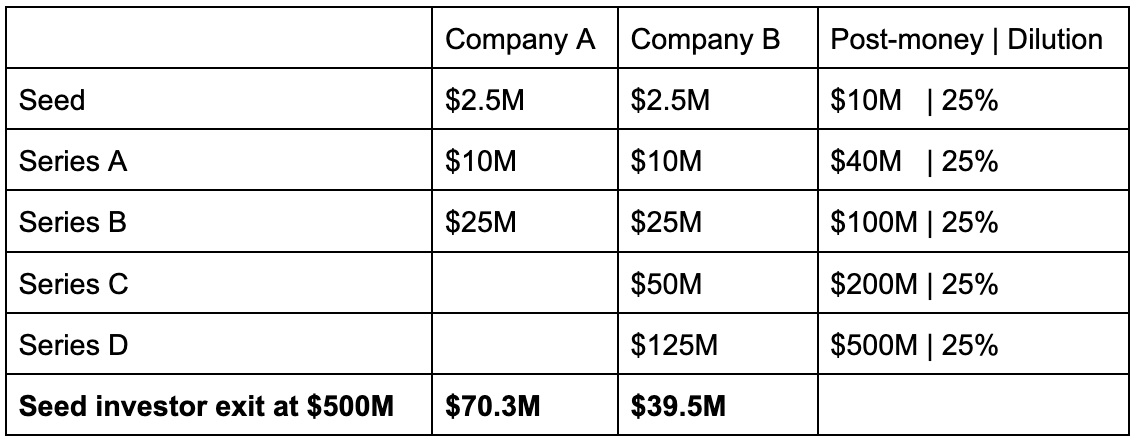

If you are building a business in a market where venture is nascent, your company should be able to scale more capital efficiently. Venture financing rounds generally come with 25% (or more) in dilution. To seed investors, the difference between a company that raises three rounds vs. five rounds is significant. Below is a comparison of a hypothetical $500M exit for a seed investor that invests $2.5M. Company A raised three rounds of funding, and company B raised five rounds. The seed investor in company A would make an additional $31M in exit proceeds, more than 12X the original seed investment. If company A raised only two rounds, the seed investor would realize $54M of additional proceeds. The same goes for founders and employees who ultimately own more of what they built!

We understand the concept of "it takes money to make money," but we also believe in the importance of disciplined thinking around capital raising. There's a current paradox, however. Venture capitalists often equate progress with companies raising new funding rounds at ever-increasing valuations. This creates a flawed system where raising capital is seen as an essential step, regardless of its impact on long-term value creation.

We believe that the "forcing function" of continuing to raise capital is a practice from a specific time period (the last decade) and markets that are very different from ours. This practice needs to be examined. Just because it’s the way things have been done doesn’t mean that it’s in the best interests of founders and investors. Beyond the issue of returns, a hidden cost of too much capital is that it encourages building a bloated organizational apparatus that only knows how to operate when company coffers are flush.

To be clear, we are comfortable sacrificing short-term reported IRRs in exchange for achieving significantly higher long-term multiples of invested capital. We believe this approach aligns better with the true goals of the partnership, which is to build companies solving hard problems and generating significant financial outcomes for our partners.